Table of Contents

- Key Takeaways

- Introduction

- Background on the 2023 Survey

- How Recharge Works in the Valley

- Recharge Efforts Expanded in 2023

- Recharge Practices Are Evolving

- Managers’ Views on Barriers, Enablers, and Priorities

- Considerations for Policy and Management

- Conclusion

- Notes and References

- Authors and Acknowledgments

- PPIC Board of Directors

- Water Policy Center Advisory Council

- Copyright

Key Takeaways

Strategies to replenish groundwater basins—long used in some areas of the San Joaquin Valley—have increasingly come into focus as the region seeks to bring its overdrafted groundwater basins into balance under the Sustainable Groundwater Management Act (SGMA). In late 2023, following a very wet winter and spring, we conducted a repeat survey of local water agencies about their recharge activities and perspectives, building on a similar survey at the end of 2017, a year with similar levels of precipitation. We found signs of progress on recharge since 2017, as well as areas where more work is needed to take full advantage of this important water management tool.

- Recharge efforts expanded in 2023. Survey respondents recharged 5.3 million acre-feet (maf) within their service areas, and we estimate that the total volume recharged valley-wide was 7.6 maf, an increase of 17 percent over 2017. More local agencies appear to be engaging in recharge, including new groundwater sustainability agencies that are managing areas that use only groundwater. Such areas often have great demand for recharge to address overdraft, but their lack of access to surface water and conveyance systems puts them at a disadvantage for recharge.

- Recharge methods are evolving. Investments have grown in dedicated recharge basins; as in 2017, they captured more than half of all reported recharge. Second in amount of water recharged, and growing, was the longstanding practice of letting aquifers replenish by replacing groundwater use with surface water (“in-lieu recharge”). Spreading water on cropped or fallowed farmland—a relatively new and cost-effective approach—has been increasing also, but still accounts for less than 10 percent of recharge volumes.

- Local and state policies have bolstered recharge efforts. At the local level, better groundwater accounting has facilitated the tracking of recharge, and some agencies are providing incentives for landowners—such as pumping credits—to support the expansion of recharge on farmland. Managers also cited local advance planning as an important enabler in 2023, especially for areas with little or no access to surface water. Two state policies—both put in place in the midst of winter and spring flooding—also got high marks: an executive order authorizing the diversion of flood flows for recharge without a water right permit, and support for acquiring temporary equipment to divert floodwater from rivers and streams.

- Local and state efforts will also be key to further progress. The state should prioritize work that will clarify when and how much water can be diverted safely, using watershed-scale assessments that consider effects on downstream water users and the environment. For locals, continued progress on the fundamentals of groundwater management—including developing strong accounting and crediting systems—will support recharge while helping to meet other SGMA goals. State and local agencies should work together to identify key infrastructure needs (including regional conveyance), refine recharge tools, secure funding, and build partnerships to expand the benefits of recharge projects.

Introduction

Groundwater recharge is an important water supply strategy across California—and especially in the San Joaquin Valley, where many groundwater basins need to address significant overdraft to comply with the 2014 Sustainable Groundwater Management Act (SGMA). Managed groundwater recharge entails intentional actions to replenish underground aquifers, using methods such as spreading water on farmland, switching to surface water so that groundwater can remain unpumped, and building dedicated basins where water can more easily percolate into aquifers. Recharge is already a long-established practice in some parts of the valley, and with the advent of SGMA it has come into greater focus. In their first groundwater sustainability plans (GSPs), submitted in early 2020, the valley’s local groundwater sustainability agencies (GSAs) identified recharge as the single biggest solution for bringing basins into balance. In total, they anticipated expanding recharge by an average of roughly 1 million acre-feet per year—across both wet and dry years—or about half of the region’s groundwater deficit (Hanak et al. 2020).

However, numerous technical and institutional constraints could prevent GSAs and their members from accomplishing this goal. Rechargers need the physical capacity to divert and capture additional water during wet periods, authorizations from regulatory agencies, and the right incentives and accounting systems to track and credit those who invest in recharge. And because dozens of GSAs and other water management agencies in the San Joaquin Valley operate in a largely decentralized manner, it can be difficult to track progress on recharge and understand where the key challenges lie.

In the fall of 2017, we surveyed 202 urban and agricultural water management agencies in the San Joaquin Valley to understand their recharge activities during 2017, the first wet year following SGMA’s passage and one of the wettest on record in the northern part of the valley. Our report Replenishing Groundwater in the San Joaquin Valley (Hanak et al. 2018) found strong interest in the practice, along with a number of issues limiting its expansion, including the availability of regional conveyance and diversion equipment to get water to recharge sites, low uptake of the relatively new technique of spreading water on farmland, regulatory barriers, and weak or nonexistent groundwater accounting systems.

Since 2017, the GSAs have begun to operate and implement their GSPs, and two further wet winters and springs (2019 and 2023) have offered additional opportunities to put groundwater recharge into practice. The state has also increased its attention to recharge. The Newsom administration identified recharge as a priority for adapting to drought and the changing climate in its 2022 California’s Water Supply Strategy (Office of Governor Newsom 2022), and state agencies have sought to support local recharge efforts with measures including temporary permitting of high-flow diversions, over $120 million in grants for recharge projects, and emergency funding in early 2023 to support the diversion and recharge of floodwaters.

This report discusses the results of a repeat survey we conducted in fall 2023. Our goal was to understand recharge activity in 2023—one of the wettest years on record in the southern valley—and identify areas of progress made since 2017, as well as remaining barriers to expanding this practice.

Background on the 2023 Survey

Both our 2017 and 2023 surveys sought to reach all local agricultural and urban water management agencies operating on the San Joaquin Valley floor. The context has changed in one key way since 2017, however: single- and multi-member GSAs now have jurisdictional coverage over this entire area, which includes 15 groundwater subbasins subject to SGMA. This means that areas that were not represented by local agricultural and urban water suppliers in our 2017 survey are now represented by GSAs. These lands—sometimes referred to as “white areas” or “undistricted lands” because they are generally not served by local water districts—typically rely almost entirely on groundwater. In some of these areas, groundwater pumpers have formed their own GSAs or management areas, and in others, counties have taken on this responsibility. GSAs are now taking on activities to track, invest in, and incentivize groundwater recharge, potentially in a more coordinated way than has been possible in the past.

As in 2017, valley water managers engaged strongly with our 2023 survey. Of the 279 agencies surveyed in 2023, we received responses representing 128 agencies (46%)—including 45 responses for individual agencies, and 14 responses for multi-member GSAs (representing 83 member agencies). This is a slightly higher overall response rate than in 2017, when we received responses from 81 individual agencies (40%).

We again received responses from agencies across the region, and from a range of different types of agencies. This time, we got better representation from agencies in the northeastern part of the valley and less representation from the southwest. We also got more responses representing agencies with little to no surface water, which reflects the expansion of agency representation in these areas under SGMA. That said, as in 2017, responses likely over-represent agencies that are active in groundwater recharge, and particularly those with large, formal recharge programs.

In this report, we summarize key survey responses, compare them with results from the 2017 survey, and provide input from a focus group discussion we held with survey respondents in spring 2024. More detail on the survey instrument and administration, sample characteristics, and additional data analysis is available in the technical appendix to this report.

How Recharge Works in the Valley

Groundwater recharge spans a spectrum of approaches, from passive to active (see text box). On the passive end of the spectrum, some surface water seeps into the ground every year—even during droughts—as a natural by-product of irrigating fields and urban landscapes and as water moves through rivers and unlined canals. On the active end, some local agencies have invested in dedicated infrastructure, such as recharge basins on lands with good permeability. Many agencies operate somewhere in the middle of the spectrum, taking advantage of opportunities to recharge extra water in unlined canals and riverbeds and on irrigated lands when it is available. Historically, such relatively informal methods were most common, and often encouraged by water agencies through price incentives that made surface water cheaper than groundwater pumping (Hanak et al. 2011). Starting in the 1990s, agencies in some areas began adopting more formal programs and accounting systems. Some of these programs are set up as groundwater banks that offer recharge services for off-site parties who have more limited opportunities on their own lands. Over time, investments in canal lining and more efficient drip irrigation systems have also restricted the use of the more traditional, passive recharge approaches in some areas.

Much of the San Joaquin Valley has characteristics that are especially suitable for recharge. For one, soils in many areas—especially on the valley’s eastern side—tend to be highly permeable. For another, intensive groundwater use and overdraft have created room to store water underground in many basins. And with SGMA’s mandate to attain groundwater sustainability, agencies in overdrafted basins now have strong incentives to recharge to bring their basins into balance. As Figure 1 shows, basins on the valley’s eastern side, including Kern, have some of the most suitable soils for recharge, as well as the largest levels of overdraft. These are also the areas where we are seeing much of the region’s recharge activity.

The eastern and southern parts of the valley face the most overdraft—and are also the most suitable for recharge

SOURCES: Recharge suitability: University of California, Davis Soil Resource Lab, Soil Agricultural Groundwater Banking Index (2015) (modified version). Subregional overdraft: Escriva-Bou et al. (2023).

NOTES: The maps depict the San Joaquin Valley’s two hydrologic regions, including headwaters (gray) and valley floor (tan), and divide the 15 groundwater basins on the valley floor into five subregions: the northeast (NE) includes Eastern San Joaquin, Modesto, Turlock, Merced, Chowchilla, and Madera basins; the southeast (SE) contains Kings, Kaweah, and Tule groundwater basins; Kern (KR) contains the Kern and White Wolf basins; the southwest (SW) contains Tulare Lake and Westside basins; and the northwest (NW) contains the Delta-Mendota and Tracy basins. In the left panel, bars summarize PPIC’s estimates of subregional overdraft using data from groundwater sustainability plans for the years 2003–10 (see Escriva-Bou et al. 2023 for details). In the right panel, blue lines represent major rivers, an important source of recharge water in wet years. Purple lines indicate major water conveyance infrastructure for the Central Valley Project and the State Water Project. The measure of recharge suitability in the right panel shows the suitability of soils for recharge if all soils with restrictive layers that would inhibit recharge were modified by deep tillage, a practice common for some crops. Depth to groundwater and permeability of sub-soil geology are additional factors influencing the suitability of a given area for recharge.

Recharge Efforts Expanded in 2023

Water years 2017 and 2023 both followed intense, multi-year droughts, and both were banner wet years in the San Joaquin Valley, creating ample opportunities for recharge. Looking across the entire valley, the total volume of precipitation was remarkably similar, though with some regional differences. The 2017 water year was the second wettest on record in the northern half of the valley (known as the San Joaquin River hydrologic region) while 2023 was the second wettest in the valley’s drier, southern half—the Tulare Lake hydrologic region (see maps in Figure 1). Indeed, 2023 brought so much water to this part of the valley that it saw the reappearance of the ancestral Tulare Lake for the first time since the late 1990s—inundating tens of thousands of acres of farmland and threatening several communities with flooding. The winter and spring storms also brought flooding and damage to infrastructure and homes in the northern part of the valley. Managers in both the northern and southern valley reported that they were often scrambling to manage flooding issues alongside recharge efforts early in the season, given the intensity of conditions on the ground.

Of course, the ability to capture and recharge additional water from winter and spring storms depends on a range of factors besides the volume of precipitation—including the timing and intensity of the storms and their runoff, as well as the capacity and readiness of potential rechargers to take advantage of the opportunity. The fact that 2023 was a relatively cold year may have created some hydrologic advantages for rechargers compared to the relatively warm 2017; a slowly melting snowpack can stretch recharge opportunities further out in the season.

Local agencies also had done more recharge planning as part of implementing groundwater sustainability plans, which might be expected to boost recharge in 2023 relative to 2017. In addition, the state had made recharge a greater funding and regulatory priority in the years leading up to 2023, and in the midst of the 2023 storm season it took two actions directly focused on expanding recharge in real time: improving the availability of pumping equipment and issuing executive orders authorizing recharge of flood flows without permits.

Sample differences between our two survey years prevent us from precisely comparing the volumes of recharge activity in the two years, but responses suggest that recharge efforts have expanded.

- More agencies are recharging. In 2017, three-quarters of agencies responding to our survey (75%) reported engaging in some recharge activity. In 2023, that share was slightly higher (79%), even though we received responses from more agencies with little or no regular access to surface water—which puts them at a disadvantage for recharge.

- Recharge volumes are higher. Respondents who were tracking volumes reported recharging a total of 5.3 maf in 2023. Based on the characteristics of the agencies that responded to the survey, we estimate that total on-site recharge valley-wide was about 7.6 maf. This represents a 17 percent (or just over 1 maf) increase in recharge volumes relative to 2017—a healthy increase in a very wet year, but likely falling short of the 1 maf average increase across wet and dry years planned for in the region’s GSPs. Nevertheless, as we explain later, some water that could have been used for recharge was likely still left on the table.

In other respects, many of the patterns we found in the 2017 survey persisted.

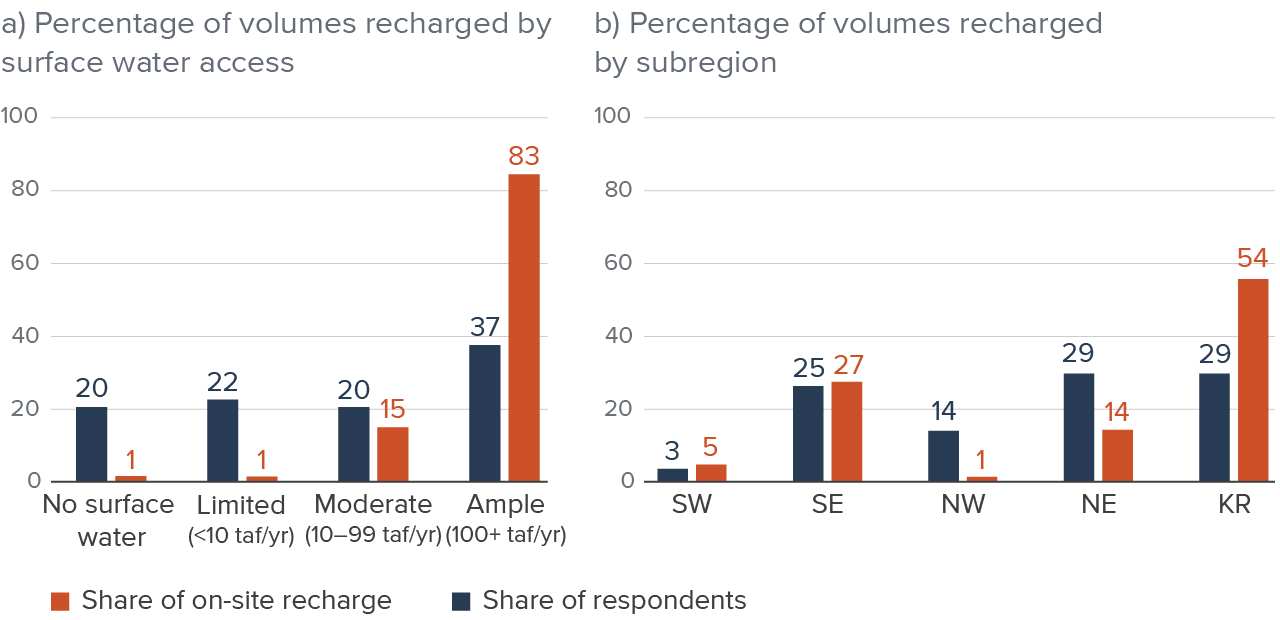

- Surface water access remains a major driver of recharge capacity. Lack of surface water often means more limited access to recharge water and conveyance infrastructure to move water to suitable locations. Agencies with relatively ample access to surface water (average annual supplies of at least 100,000 acre-feet [af]) were responsible for the lion’s share of reported recharge (83%, up from 79% in 2017); those with little to no surface water increased their recharge, but still accounted for just 2 percent of the total (Figure 2a). Recharge remains a major priority on these lands, which often face the greatest potential pumping cutbacks as SGMA implementation proceeds (Hanak et al. 2023).

- Kern and the southeast still lead the way. As in 2017, the Kern basin—home to many longstanding groundwater banks—led the way with 2.9 maf of on-site recharge (54% of the total volume reported), followed by the southeast region with 1.4 maf (27%) (Figure 2b). These are nearly identical proportions to 2017. What’s new is a large uptick in the northeast, with more than 0.7 maf of on-site recharge—nearly triple the volume reported in 2017. As described above, all three of these regions have relatively favorable recharge conditions, and a strong demand for recharge to address groundwater overdraft (Figure 1).

- Agricultural agencies recharge much more than cities. Many of the valley’s urban agencies are beginning to engage more actively in recharge partnerships to help shore up their supplies, and most reported some engagement in recharge activities in 2023. But agricultural agencies accounted for most of reported on-site recharge—5.1 maf —versus just 0.2 maf for urban agencies. This discrepancy reflects agricultural agencies’ much larger demand for water, as well as their better access to both surface water and suitable recharge lands.

Agencies with ample surface water recharged the most water in 2023, and Kern and the southeast were regional leaders

SOURCE: PPIC San Joaquin Valley 2023 groundwater recharge survey.

NOTES: The figure shows the distribution of the 59 survey respondents (45 individual agencies and 14 multi-party GSAs representing 83 member agencies) (blue bars) and the distribution of total on-site recharge reported (5.3 maf) (orange bars). To avoid double-counting, we exclude off-site recharge, which could be reported by both partners. Blue and orange bars each sum to 100 percent in each figure. The volume of surface water is the annual average of water deliveries to the agency (see Technical Appendix A for details). Taf/yr is thousands of acre-feet per year. SW is southwest, SE is southeast, NW is northwest, NE is northeast, and KR is Kern. In all, 33 respondents reported recharge volumes.

Recharge Practices Are Evolving

Beyond the question of how much recharge occurred, the survey sheds light on how recharge practices are evolving in the SGMA era. Here we review recharge methods, sources of water used, and how local agencies are tracking and accounting for recharge and providing incentives to landowners.

Agencies Are Using a Similar Portfolio of Recharge Methods as in 2017

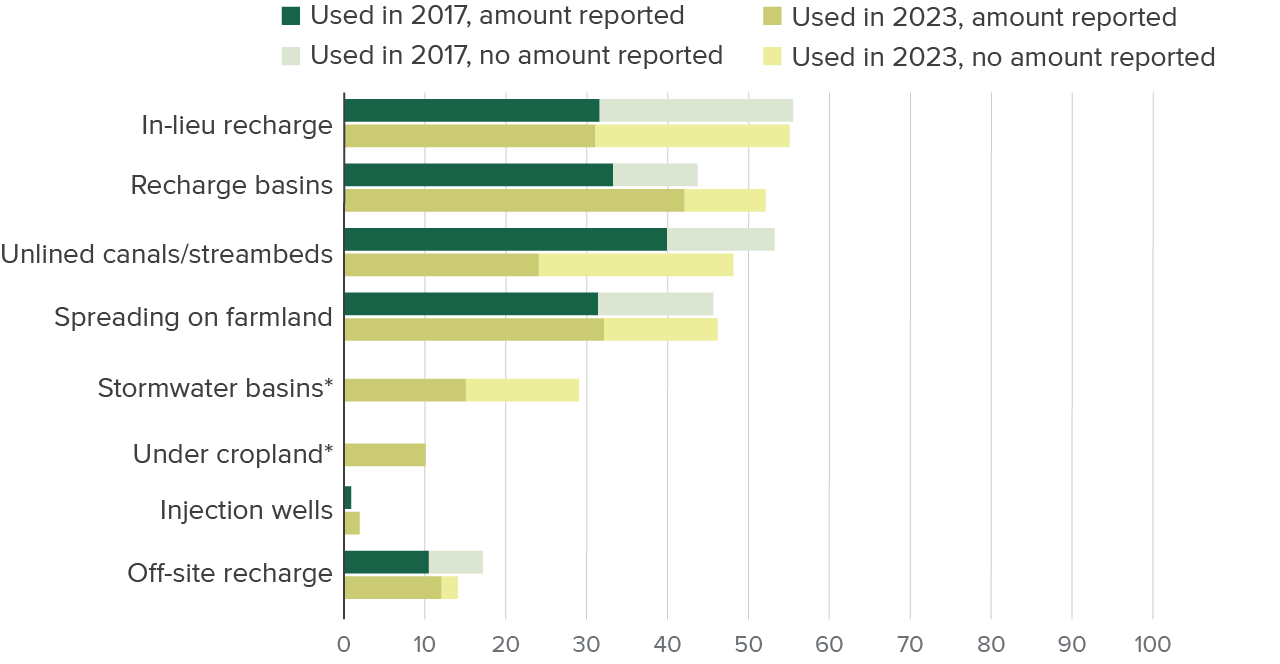

We might expect some changes in the landscape of recharge practices since 2017 given GSAs’ plans to expand recharge capacity as part of their groundwater sustainability plans. The recharge projects in those plans emphasized recharge basins and in-lieu recharge activities (Jezdimirovic et al. 2020). There have also been considerable efforts in recent years to disseminate information about the relatively new method of recharging by spreading water on active or fallowed cropland, floodplains, and other open space.

On balance, while over half of all survey respondents said they expanded their recharge capacity since 2017, there was little change in the overall prevalence of various recharge methods. Four of these were used by about half of all respondents in both years: in-lieu recharge, recharge basins, unlined canals and streambeds, and spreading water on farmland (Figure 3). Several agencies also reported using two methods that we first asked about in the 2023 survey. Stormwater basins, which can be used for recharge, are especially popular with urban agencies that operate these as part of their flood control systems. And some agricultural agencies are experimenting with recharging using perforated pipes under active cropland—a technique that has higher up-front costs but offers more control to the grower than spreading water on farmland.

As in 2017, agencies were less likely to track and report volumes recharged by spreading water on farmland or by using the more traditional or passive methods—in-lieu, unlined canals, and stormwater basins. In the case of recharge on farmland, agencies can either apply water to the land on their own behalf (for example, by leasing land from growers to use for recharge), or deliver water to landowners with the assumption that it is being spread for recharge. The latter practice is more difficult to track and monitor, which may partly account for the lower volumes reported for this method. In contrast, volumes stored in recharge basins or as part of off-site banking partnerships were much more likely to be tracked (Figure 3).

Roughly half of all local agencies use four main recharge methods—in-lieu recharge, recharge basins, unlined canals, and spreading water on farmland—but tracking and reporting of recharge amounts remain spotty

% of respondents

SOURCES: PPIC San Joaquin Valley 2017 and 2023 groundwater recharge surveys.

NOTES: On-site methods are shown in order of their prevalence in 2023, from largest to smallest; off-site recharge is most commonly done at groundwater banks that use recharge basins. Asterisks indicate categories that were new to the 2023 survey. Spreading water on farmland includes recharge on active cropland and fallowed land, as well as a small amount of water recharged on open space/floodplains. See the text box for descriptions of the various recharge methods. In 2017, we received responses from 81 individual agencies, and in 2023 we received 59 responses, including 45 from individual agencies and 14 from multi-party GSAs (representing 83 member agencies).

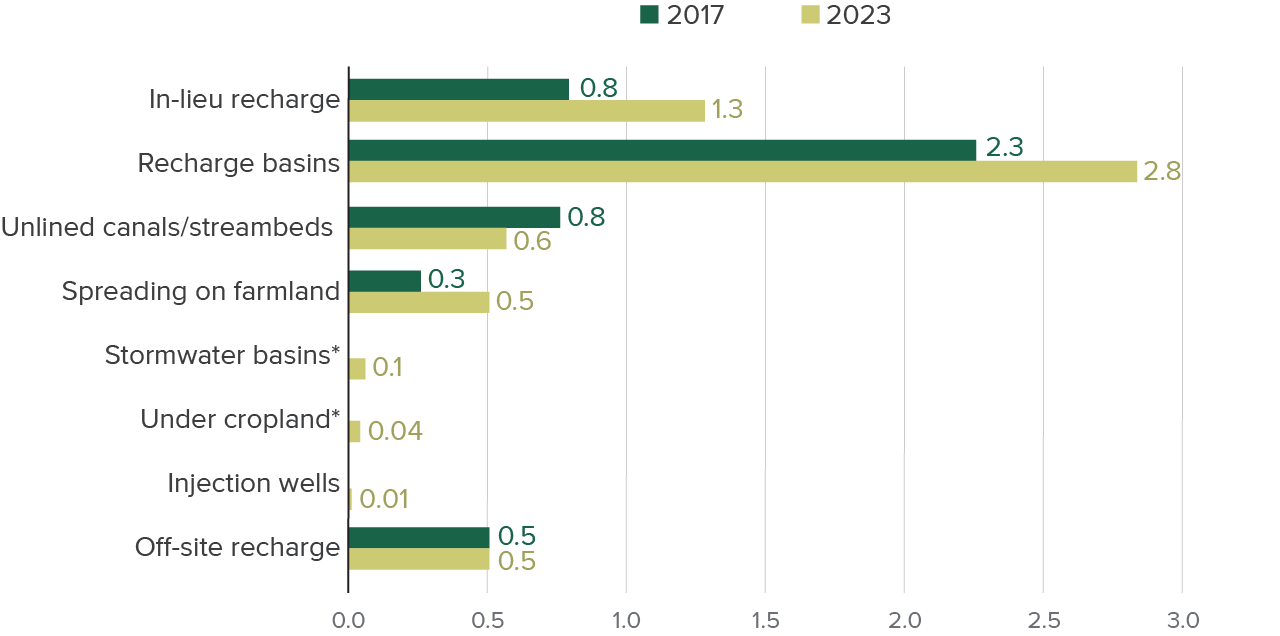

Some Methods Are Capturing Much More Water than Others

Even allowing for differences in reporting, it’s clear that the four widely practiced recharge methods are playing quite different roles. As in 2017, dedicated basins accounted for more than half the volumes recharged (Figure 4). In-lieu recharge volumes grew, but came in a distant second, with nearly a quarter of the total. Spreading water on farmland also grew, though tracked volumes remain small (9%). Finally, recharging water in unlined canals and streambeds (11%) was the only one of the four most widespread methods that saw a dip—perhaps reflecting less tracking of this method in 2023.

As in 2017, more than half of the water applied for recharge in 2023 was spread in dedicated recharge basins

Millions of acre-feet

SOURCES: PPIC San Joaquin Valley 2017 and 2023 groundwater recharge surveys.

NOTES: The 2017 survey included 46 respondents who reported recharge volumes. The 2023 survey included 33 respondents who reported recharge volumes, including eight primarily agricultural GSAs (representing 41 member agencies), 22 individual agricultural agencies, and five urban agencies. In 2017, reported on-site recharge totaled 4.1 maf and off-site recharge totaled 0.5 maf. In 2023, reported on-site recharge totaled 5.3 maf and off-site recharge 0.5 maf. Most off-site recharge is likely included in the on-site volumes reported by recharge partners. The “spreading on farmland” category includes recharge on active cropland, fallowed land, and open space lands; the latter accounts for about 5 percent of the volume applied on farmland in 2023 (493 taf) and 14 percent of the volume in 2017 (260 taf). Asterisks indicate categories that were new to the 2023 survey.

In comparison, the three other on-site recharge methods—via stormwater basins, running water through tile drains under cropland, and injecting water into wells—barely register. Whereas the latter two methods are closely monitored, the small numbers for stormwater basins could partly reflect challenges in tracking volumes stored.

Finally, off-site recharge, which generally involves formal banking of water by one party on behalf of another, saw similar volumes in both years, despite the overall growth in on-site recharge. A total of seven respondents (12%) reported banking 536,000 acre-feet for their customers in off-site projects; most of this (88%) occurred through recharge partnerships among parties in the Kern subregion. It is possible that some respondents did not report other local partnerships—particularly when they occur within GSAs that responded as a group. Nevertheless, the apparent lack of growth in groundwater banking partnerships could represent a missed opportunity for agencies that do not have suitable or adequate recharge capacity on their own lands.

Rechargers Tapped More Water Sources in 2023

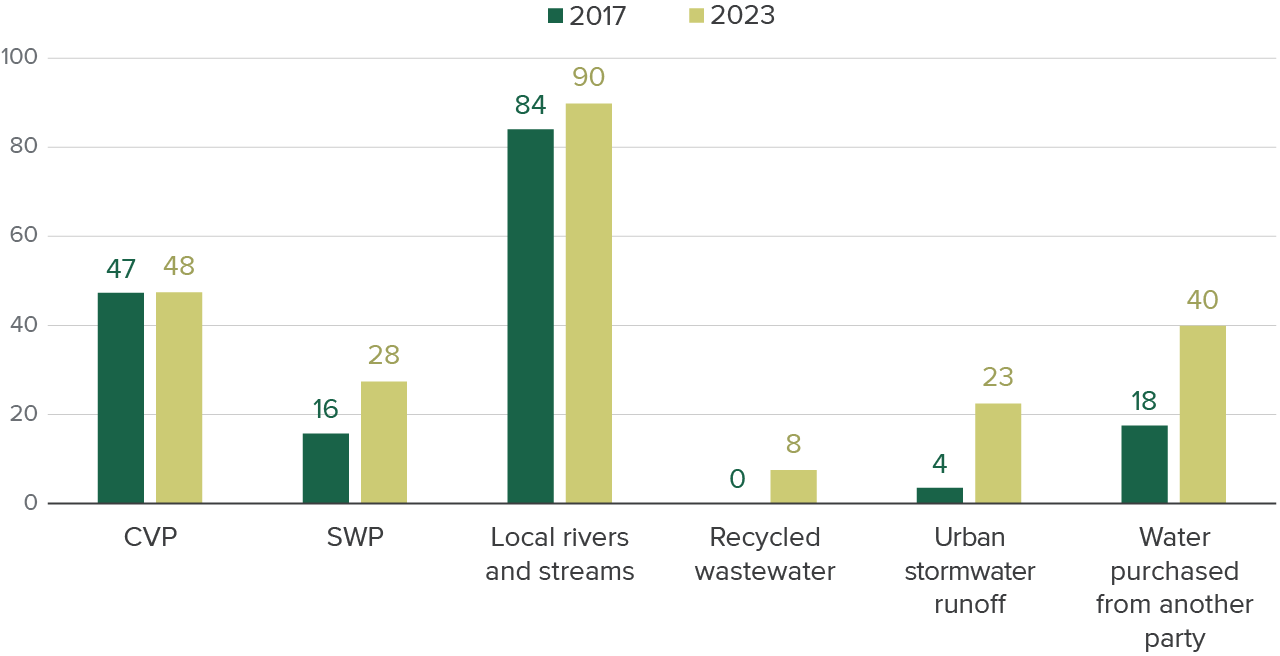

The main sources of water for recharge remained largely similar to those reported in 2017, with agencies drawing on water from local rivers and streams, imported water—including both regular deliveries and flood flows—from the Central Valley Project (CVP) and State Water Project (SWP), and both local and imported water purchased from other parties (Figure 5). But as water agencies increased their recharge activity, they leaned more heavily on some of these sources and started tapping some new types of supplies.

- Local rivers and streams—including floodwaters—remained a major source. Local rivers and streams on the valley’s east side—shown in Figure 1 above—supply many agricultural water agencies with irrigation water, and during wet years they serve as a major source for recharge. In 2023, flooding conditions increased both the challenges and opportunities provided by these local waters. A full 90 percent of respondents reported using local water for recharge, up from 84 percent in 2017. Several agencies received a significant influx of recharge water from flooding, and the Newsom administration’s executive orders (EOs) in the spring of 2023 (Executive Order N-4-23 and Executive Order N-7-23) granted local agencies and landowners permission to divert floodwater onto their land for recharge without water right permits. More than a quarter of respondents indicated that the EOs enabled more recharge in 2023; one GSA reported that 90 percent of recharge water applied by their members was diverted via EO N-4-23.

- A market for recharge water is developing. Even in a very wet year, not everyone has ready access to water for recharge; one solution is to buy it from others. In 2023, a much larger share of respondents (40%) purchased recharge water than in 2017 (18%). Managers told us that the market for recharge water has been growing in recent years—in addition to the regular irrigation season market, there is now a market for recharge water in winter/early spring, and even in the fall in some years. While these trends may create opportunities for some parties to expand recharge, they also raise the price of recharge water for those who were accustomed to getting this water with less competition in the past.

- Urban recharge sources are on the map. Both urban stormwater and recycled water now appear as recharge sources for some urban and agricultural agencies—a change since 2017, when few if any agencies reported them. While still not widespread, the growth in these sources reflects interest in tapping a variety of local sources for recharge—even in wet years—and a rise of urban–agricultural partnerships.

Water from local rivers and streams was the most common source for recharge in both 2017 and 2023

% of respondents

SOURCES: PPIC San Joaquin Valley 2017 and 2023 groundwater recharge surveys.

NOTES: The 2017 sample includes 57 responses from agencies that reported recharge sources: 48 agricultural agencies and nine urban agencies. The 2023 sample includes 40 responses from agencies reporting recharge sources: 10 primarily agricultural GSAs—representing 60 member agencies—and 30 individual agencies (23 agricultural and 7 urban). One 2023 respondent who reported recharge sources did not have an active recharge program in 2023. CVP is the Central Valley Project; SWP is the State Water Project.

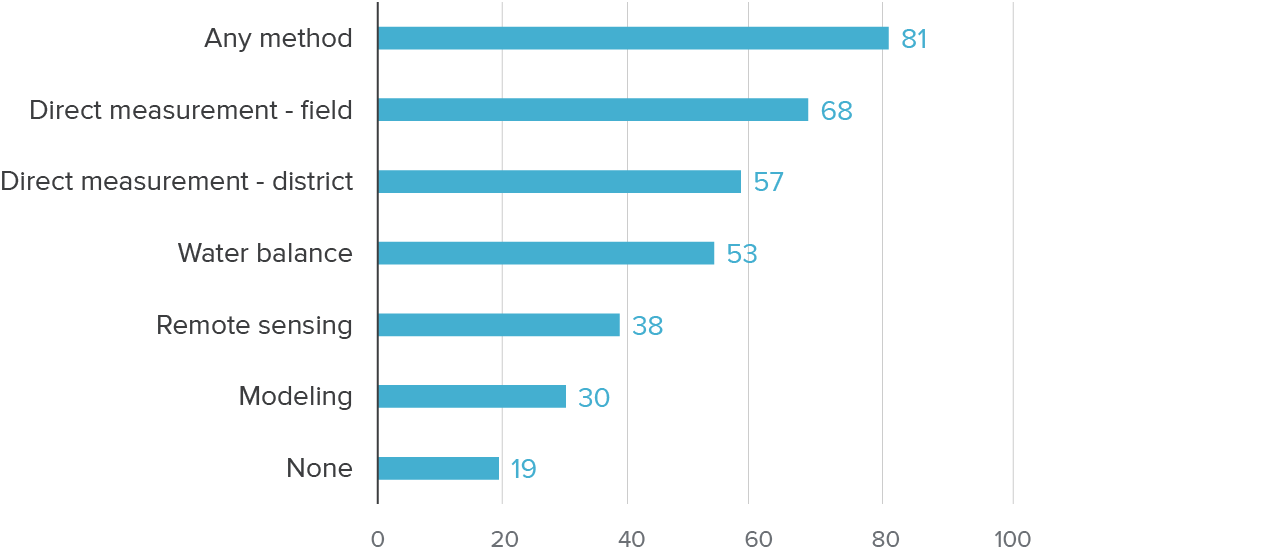

Groundwater Accounting Is Advancing, and It Is Essential for Tracking Recharge

SGMA is ushering in a new era of water accounting in California’s groundwater basins, and the valley is no exception. While some valley agencies already had relatively advanced systems for tracking aquifer inflows and outflows prior to SGMA’s enactment, the law requires that basins develop unified groundwater budgets and regularly monitor changes in groundwater use, storage, and other metrics. This requirement has forced virtually every agency to up its game. Our 2017 survey identified addressing accounting gaps as a major priority for advancing recharge in the valley. Strong accounting systems help incentivize parties to collaborate on recharge projects that provide basin-wide benefits, and to credit those who are bearing the costs of recharge, such as landowners. Strong accounting—and the development of groundwater allocation systems—will also be critical to managing demand in basins that will need to reduce pumping.

To get a sense of advances in recharge accounting, we added some questions about accounting systems to the 2023 survey. Figure 6 shows five groundwater accounting methods that rechargers reported using to quantify and manage recharge, including directly measuring at the field or the district level, tracking water balances, measuring water use via remote sensing, and using hydrologic modeling techniques. The good news is that most of these agencies (81%) were using at least one accounting method, and two-thirds (66%) said they employed two or more methods. Tellingly, agencies that reported recharge volumes for 2023 were using at least one—and usually multiple—accounting methods.

Still, a fifth of active rechargers reported having no accounting framework at all. Many of these have primarily used recharge methods that are less commonly tracked, such as in-lieu recharge or spreading water on farmland, or did not yet have a fully developed recharge plan. As we describe later, strengthening accounting systems is a key area for improvement if recharge efforts are to continue expanding in the future.

Groundwater accounting methods in use by rechargers in 2023

% of respondents

SOURCE: PPIC San Joaquin Valley 2023 groundwater recharge survey.

NOTES: The sample includes 47 respondents who reported active recharge programs in 2023, including 11 primarily agricultural GSAs (representing 63 member agencies), 26 individual agricultural agencies, and 11 urban agencies. Three additional respondents reported use of groundwater accounting methods in 2023 but did not have active recharge programs. Direct measurement at the field level includes flowmeters at turnouts; direct measurement at the district level includes flowmeters at headgates and well level monitoring; water balance refers to tracking water inputs and outputs to understand net use; remote sensing includes satellite or near-ground (e.g., drone, aerial) imagery methods for estimating evapotranspiration or other metrics of water use; and modeling refers to computer-simulated estimates of hydrological balance.

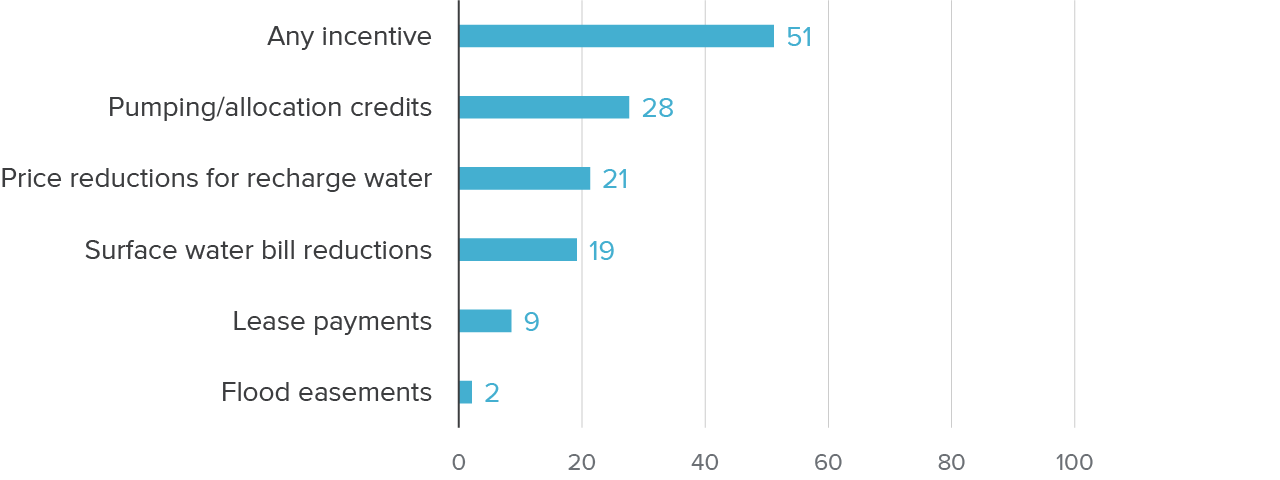

Local Agencies Are Launching Recharge Incentives for Landowners

As interest grows in spreading recharge water on farmland, it’s important to offer landowners the right incentives to take on these efforts. Growers wishing to divert floodwater onto their land incur costs, especially if they must install a meter, maintain dual-use irrigation systems (e.g., both inefficient “flood” systems to be able to rapidly apply high volumes of water, and more efficient drip or micro-sprinkler systems for the main irrigation season), reinstall checks and turnouts, or hire additional labor to maintain and monitor pumps and siphons. Many are reluctant to do so unless they can be guaranteed later use of some portion of the water applied. Similar issues arise in places where landowners are setting up their own recharge basins; at a minimum, they need to cover the costs of the investment (including the water), and they generally will want credits for at least some of the water they recharge.

A strong groundwater accounting system that includes pumping allocations for individual farms will incentivize landowner recharge because it simplifies the process for providing rechargers with pumping credits. Over a quarter of active rechargers—and half the agencies where growers are recharging by spreading water on farmland—reported using pumping credits to encourage recharge in 2023, the most of any incentive mechanism (Figure 7). These crediting programs allow growers to use the water at a later time, and they typically follow rules of thumb for how much applied water is likely to percolate to the aquifer as recharge, with the understanding that these ratios can be adjusted as information improves. Some landowners and agencies are even partnering up to accept water for recharge as part of good-faith negotiations, where landowners may bank credits in anticipation that the agency will adopt an allocation scheme in the future.

We also inquired about financial incentives, including price reductions for recharge water (used by 21% of active rechargers), surface water bill reductions to incentivize in-lieu recharge (19%), and lease payments to use the landowner’s property for recharge (9%). Only one agency reported using temporary flood easement agreements with landowners to facilitate spreading water on these lands, but several others told us that they were paying growers to “farm with water” on fallowed land. In all, half of active rechargers—and more than two-thirds of those with programs to spread water on farmland—reported using at least one type of incentive, and these practices are likely to grow. For instance, several agencies said that they were planning on developing credit policies, and several are looking at developing a suite of the incentives listed here.

Incentives for landowners are still developing, and pumping credits are currently the most widespread

% of respondents

SOURCE: PPIC San Joaquin Valley 2023 groundwater recharge survey.

NOTES: The sample included 47 respondents who reported having active recharge programs in 2023: 11 primarily agricultural GSAs (representing 63 member agencies), 26 individual agricultural agencies, and 10 urban agencies. Three rechargers reported using other incentives than the categories shown here (payments to landowners to recharge on fallowed land and requirements to pay for surface water allocations even if the landowner doesn’t use them). Two agencies that reported not having an active recharge program in 2023 also used groundwater pumping or allocation credits, likely as part of their groundwater management activities.

Managers’ Views on Barriers, Enablers, and Priorities

Expanding recharge requires many things to come together beyond favorable weather: the availability of suitable areas for recharge and the requisite equipment and infrastructure, regulatory approvals for diverting the water and building recharge projects, strong monitoring and accounting systems to track and incentivize recharge, the right set of partners, and the funding needed to cover project expenses. We asked managers to give us their insights on what was especially helpful in 2023, what’s been getting in the way of doing more recharge, and their priorities for expanding recharge in the years ahead.

Recharge Was Up in 2023, but Even More Might Have Been Possible

As context for this discussion—given the large volumes recharged in 2023—it is worth considering how much more water might have been available for capture and storage underground. We did a rough estimate, looking at water flowing out of the San Joaquin River into the Delta that was not required to meet environmental standards or the needs of other water users. We found that another 3.5 million acre-feet was potentially available for recharge in upstream areas, particularly between March and June. An additional 0.4 maf of Sacramento River water might also have been available for recharge in the areas that import water from the Delta. (For an updated, more detailed analysis, please see our December 2024 explainer.) While it would not be practical to capture all of this water—particularly during periods of very high flows—this suggests that there is indeed still room to grow these programs without harming the environment or other water users. Doing so could help the valley get closer to its goal of 1 million additional acre-feet of recharge on average each year, which would entail balancing out the dry years with extra water captured during abundant years like 2023.

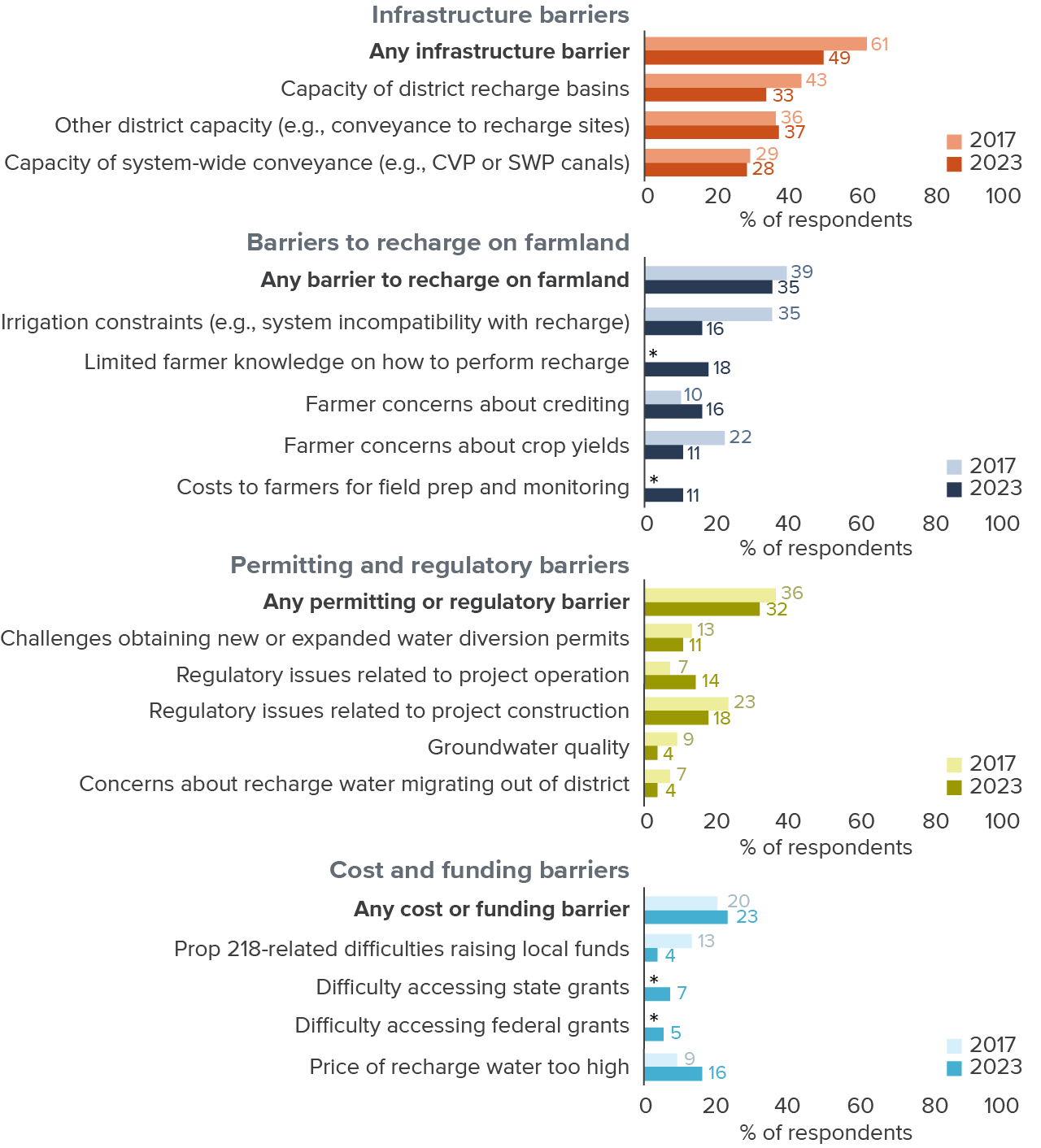

Some Limitations to Recharge Are Easing, but Many Remain

For barriers, we focused on four areas: infrastructure, spreading water on farmland, permitting and regulatory issues, and issues related to funding and costs. Managers could select as many barriers as they wanted. Figure 8 summarizes the share of respondents that picked each individual barrier and the share that picked at least one barrier in each of the four groups, comparing responses in 2017 and 2023.

Managers’ views on barriers to groundwater recharge in 2023

SOURCES: PPIC San Joaquin Valley 2017 and 2023 groundwater recharge surveys.

NOTES: The 2017 sample (lighter bars) included 69 respondents (57 agricultural agencies and 12 urban agencies). The 2023 sample (darker bars) included 57 respondents, including 13 primarily agricultural GSAs (representing 81 member agencies), 30 individual agricultural agencies, and 14 urban agencies. Asterisks show categories that were assessed in the 2023 survey, but not in 2017.

Despite progress on recharge basins, infrastructure constraints still loom large

The physical capacity of local district- and broader system-level infrastructure was a major barrier to recharge in 2017, and it continued to limit the ability of agencies to capture water for underground storage in 2023 (Figure 8). Half of all respondents encountered at least one infrastructure-related barrier to recharge, whether the capacity of district basins or other district-level infrastructure such as canals and turnouts, or the capacity and connectivity of system-wide conveyance (e.g., CVP canals and the SWP’s California Aqueduct). Managers emphasized these barriers even as the capacity of local recharge basins has improved.

Some also emphasized the important interplay between surface and groundwater storage—and noted that a lack of capacity in surface storage, which helps slow down runoff, was hampering getting more water into the ground. Indeed, nearly half of agricultural rechargers and one urban recharger reported having more recharge capacity than they were able to use, suggesting issues with the timing of surface water availability, connectivity to larger conveyance networks, or the ability to capture and hold water for recharge.

Barriers to spreading water on farmland are still present, but evolving

Managers gave barriers to spreading water on farmland the second-highest overall score in 2017, and that was also true in 2023 (Figure 8). Since 2017, some technological wrinkles appear to have been ironed out—e.g., constraints related to irrigation systems were cited less often, as were farmer concerns about inundation damaging crop yields.

This suggests that as methods for spreading water on farmland have gained traction, participants are finding solutions for technical problems, gaining familiarity with research and recommendations for safely inundating cropland, and becoming more interested in how recharge on farmland and related methods can be integrated into their water management plans.

Still, managers raised concerns about farmer know-how limiting the broader application of these methods, as well as the cost to growers for retrofitting, maintaining, and installing adequate irrigation systems for applying high-volume flows. They also reported higher levels of concern among growers about whether they will receive sufficient credit for taking water on their land, perhaps signaling both that landholder interest in these methods is growing, and that in some areas it may be outpacing the development of local programs that account for and allocate groundwater.

The regulatory environment still poses obstacles

In 2017, survey-takers identified addressing regulatory barriers as another area needing improvement. Respondents were particularly concerned about approvals to construct and operate new recharge projects and for acquiring water rights or contracts for recharge water. These issues are still on the radar in 2023 (Figure 8).

On the issue of water rights for recharge, managers recognize that there has been some progress in recent years, including an expedited temporary permit review process and streamlined guidance from the State Water Board. On the plus side, the temporary permit confers a right to the water that is recharged. According to some managers, however, the board has been hesitant to grant these permits in some places where there are fully appropriated streams, citing concerns that all the water is already spoken for.

The EOs for floodwater recharge issued in spring and early summer 2023 also proved helpful and were codified into law as part of a budget trailer bill in summer 2023 (Senate Bill 122). The EOs for floodwater recharge had the advantage of not requiring a permit, but the disadvantage of not conferring a right to the water that is recharged. This gives less certainty to rechargers, although some GSAs—the entities responsible for groundwater management—have adopted policies crediting water diverted under the EOs.

As of this writing, discussions are underway to “clean up” the language in last summer’s budget trailer bill with a new piece of legislation (Senate Bill 1390), both to clarify protections for downstream water users and the environment, and to clarify conditions under which rechargers may proceed with investments to support their recharge efforts.

As Figure 8 shows, managers cited obstacles related to project construction and operation more frequently than the water rights issue, which reflects the challenges that managers face in getting other types of approvals for their projects. In particular, managers have spoken of frustrations with a lack of coordination among different permitting agencies regarding regulatory requirements, such as installing fish screens on diversions or rules against using pumps on some canals, and concerns that these requirements are making opportunistic recharge efforts from flood flows unrealistic.

Finally, and somewhat to our surprise, managers did not cite water quality concerns as a significant regulatory barrier to recharge, even though recharge efforts must occur in a way that does not significantly degrade water quality. When we asked managers in our focus group about this, they noted that the urgency of flood control actions in 2023 took precedence. Water quality will remain an issue to tackle in planning for recharge.

The price of recharge water was the main in-the-moment financial concern

Among funding and cost barriers, managers only emphasized a single issue—the price of recharge water—as an obstacle to recharge in 2023. As noted above, the price of recharge water can be an issue in some parts of the valley, given the development of a recharge season market.

We asked respondents in our focus group about the limited emphasis on funding as a barrier. They noted that in the moment—when everyone was scrambling to avoid flooding and take advantage of recharge opportunities—managers were most concerned with how to maximize the resources they already had available. As discussed below, funding resurfaces as a priority for expanding recharge capacity in the future.

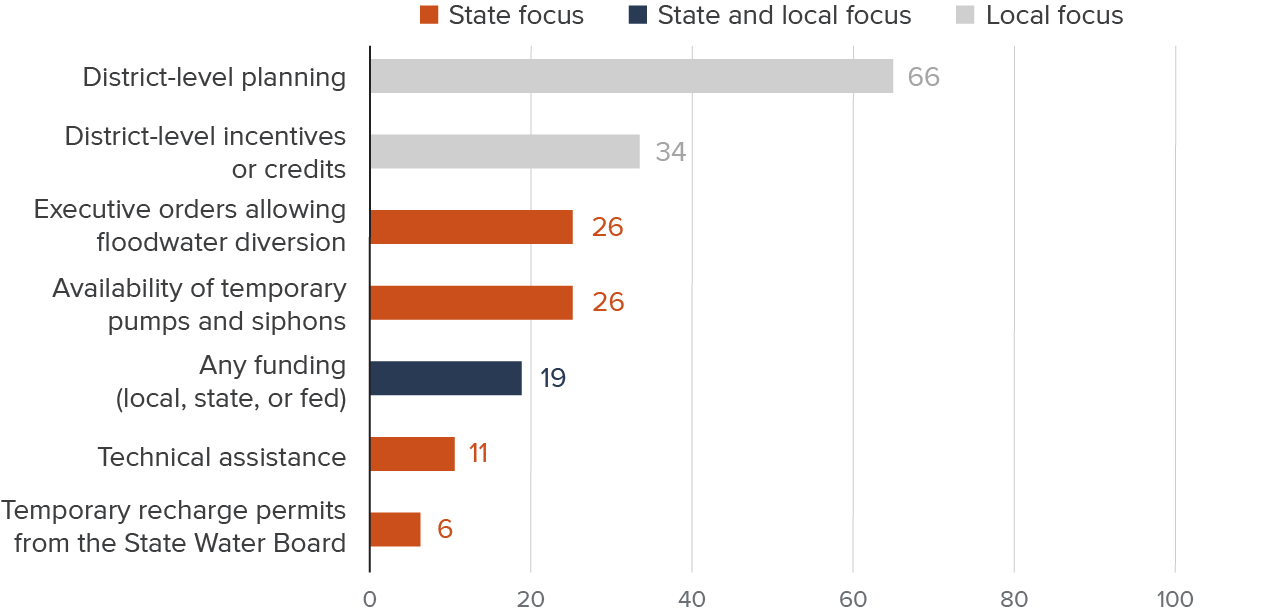

Various State and Local Efforts Enabled More Recharge in 2023

We also asked managers to tell us which factors facilitated their recharge activities in 2023. Respondents confirmed that there has been general progress in local readiness, and they highlighted the value of changes in state policy and practice that occurred in the midst of the 2023 recharge season (Figure 9). One striking result was that agencies with programs to spread water on farmland were more likely than other rechargers to say they benefited from the enablers listed below. Thus, even though these techniques are not yet responsible for large volumes of recharge, many agencies are taking advantage of opportunities to expand their use.

- Local planning and crediting programs were the most important recharge enablers. The factor most frequently credited with enabling more recharge in 2023 was local district-level planning; in all, two-thirds of all agencies with active recharge programs felt this was true for them. This suggests that the formation of GSAs as coordinating bodies, along with the development of GSPs and ongoing implementation of these plans, has enhanced the ability of water managers across the valley to proactively prepare to receive and capture more water for recharge—even in areas with little or no access to surface water. A third of all rechargers also viewed crediting programs, which encouraged landowners to recharge on their lands, as a key enabler.

- The executive orders on flood diversions were more helpful than temporary recharge permits. The executive orders facilitating the diversion of floodwaters for recharge were flagged as helpful by a quarter of respondents (26%), much higher than the share that found temporary recharge permits from the State Water Board helpful (6%). The enthusiasm for the EOs extended beyond the agencies that actually made use of them, likely reflecting managers’ appreciation of a policy innovation that relaxed regulatory requirements around accessing water for recharge, which has been a widespread concern in the region.

- The state’s efforts to make recharge equipment available were also popular. Support for acquiring temporary pumps and siphons to help increase the diversion capacity of local agencies and landowners was flagged as helpful by a quarter of respondents (26%). Managers appreciated this emphasis on rapid problem-solving to get more water onto agency and private lands.

- Funding programs were important for some agencies. One-fifth of respondents (19%) reported that government funding programs (local, state, or federal) were significant enablers of recharge in 2023. Several explained that grant programs had helped them develop recharge capacity in advance of the season.

Water managers credited a range of factors for enabling more groundwater recharge in 2023

% of respondents

SOURCE: PPIC San Joaquin Valley groundwater 2023 recharge survey.

NOTE: The sample included 47 respondents who reported having active recharge programs, including 11 primarily agricultural GSAs (representing 63 member agencies), 26 individual agricultural agencies, and 10 urban agencies.

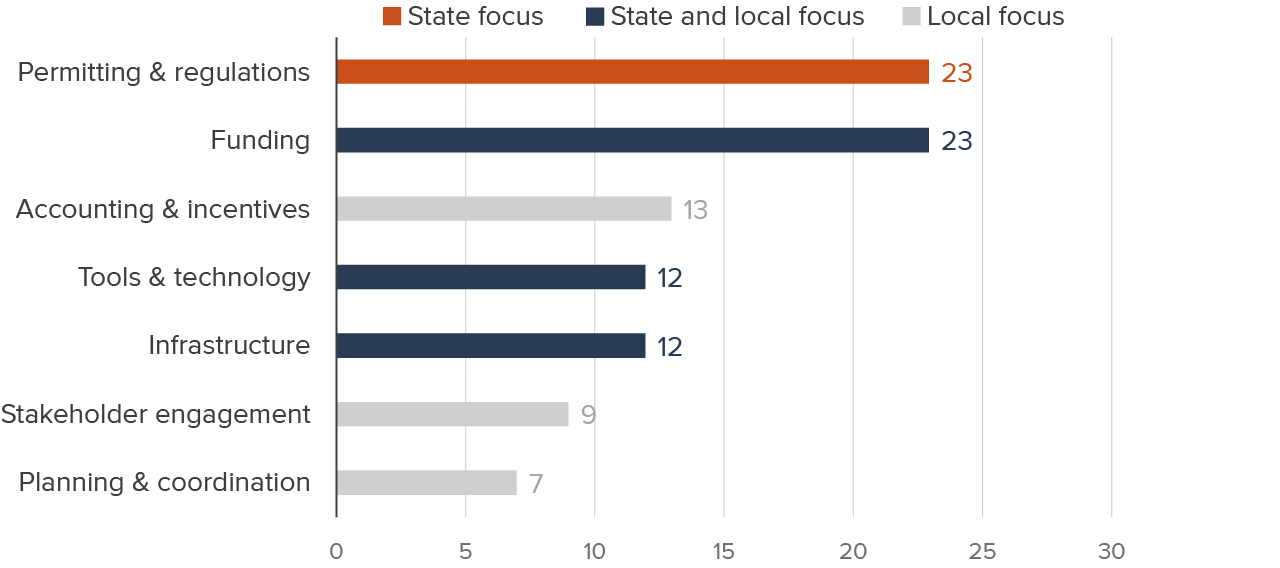

Managers Emphasized Both State and Local Priorities to Expand Recharge

Finally, we asked managers to list their top two or three priorities for expanding recharge in the future. Figure 10 summarizes these results. As with enablers, their responses flag areas for both state and local action.

- State action on the regulatory front is a top priority. Nearly a quarter of the issues raised by managers fall into this category. Not surprisingly, managers recommended continued refinement of the rules for recharging with floodwater. They also suggested streamlining and speeding up permitting for the construction of new recharge projects, as well as facilitating water transfers—an increasingly important source of recharge water. This includes consolidating the place-of-use designations for CVP and SWP water—something often done during droughts—to make it easier to use transferred water for recharge on suitable lands.

- Funding from all levels of government also rises to the top. Another quarter of the priorities mentioned pertained to increasing the availability of funding. Respondents cited the need to support the construction and maintenance of conveyance facilities and recharge basins, and the need to acquire land on which to develop new projects. While state and local governments will play the largest role here, respondents were also interested in leveraging federal funds for recharge projects.

- Continued local progress on accounting and incentive systems will be key. Managers emphasized the need to further develop accounting and crediting systems, both to facilitate groundwater banking projects and to incentivize more landowners to recharge on their lands.

- Improving local and regional water infrastructure can relieve bottlenecks. In addition to expanding local recharge facilities such as dedicated basins, many managers emphasized improving the capacity and connectivity of the regional water conveyance grid to facilitate getting recharge water to suitable areas. Conveyance investments are often regional in scope and may require state and federal involvement.

- Practical tools and technologies are needed for on-the-ground implementation. To boost future recharge efforts, managers identified the need to develop and install dual-use irrigation systems (i.e., for both flood and drip applications), ensure the availability of temporary pump stations during high-flow periods, and conduct geophysical assessments of the best places to recharge. Others pointed to the need to further develop recharge technologies such as reverse tile drainage or dry well recharge. Here again, there are roles for both state and local actors.

- More local stakeholder engagement could boost recharge on farmland. Some managers cited the need to raise awareness among landowners and others in the community, especially about the potential benefits of spreading water on farmland.

- Continued local planning and coordination are needed. Planning was a key enabler of recharge in 2023, and several managers emphasized the importance of continuing this work—for instance to assess the financial feasibility of recharge options. Managers suggested that forming recharge partnerships is another way to leverage resources and opportunities across agencies.

Managers identified a range of state and local priorities for expanding groundwater recharge

% of responses

SOURCE: PPIC San Joaquin Valley 2023 groundwater recharge survey.

NOTES: The sample included 38 respondents, including nine multi-party GSAs (representing 63 member agencies) and 29 individual agencies. Respondents could list up to three priorities; percentages reported in the figure are out of 90 total responses and they sum to 100.

Considerations for Policy and Management

When assessing the results of our 2017 survey of local water managers, we flagged six areas for policy and management attention to improve recharge opportunities in the valley. Six years later, with the benefit of new survey results, it is worth briefly revisiting these issues.

Continue Refining the Rules for Recharge Diversions

In 2017, local water managers and state officials alike wanted to better understand the conditions under which water from storms could be diverted for recharge while protecting the rights of downstream water users and the environment. There was also a clear need for the state to develop an expeditious process to enable water users to divert and recharge water when it is available.

This is still very much a work in progress. There has been movement on improving the process for enabling local agencies and landowners to make recharge diversions—both through the State Water Board’s temporary recharge permit option and the new process, following on last spring’s executive orders, for diverting water without a permit during flood emergencies. There have also been important recent advances in understanding flow issues at the watershed scale that shed light on the role recharge would play—both in altering water available for other uses and in reducing flood risk.

Nevertheless, major technical and policy questions still loom about how much water is available for recharge in different watersheds. And as interest in recharge diversions has grown, so have objections from parties concerned with potential impacts to their water rights. Making significant further progress will likely require a larger assessment process—involving multiple stakeholders at the scale of entire watersheds—to establish conditions under which recharge diversions are possible considering the range of water users and uses that depend on these waters. For the San Joaquin River and its tributaries, this effort will need to consider broader impacts on the Delta and those who draw water from it.

Ease Infrastructure Constraints

In the past six years there has been progress in local infrastructure to support recharge, especially with the expansion of dedicated basins. Some agencies are also exploring options for enhancing local surface storage to work better in tandem with recharge efforts. Surface reservoirs can temporarily hold some water, and by slowing it down, increase the capacity to get more of it into the ground.

But policymakers and managers have yet to address a major issue we identified in our last review: the capacity of conveyance systems to get water to the best places for recharge. State and regional partners should collaborate to assess where improvements in regional connectivity would be cost-effective, for instance with a new east–west connection. Federal partners would ideally join this effort as well.

Enhance Groundwater Accounting

Groundwater accounting tracks how much water goes into a basin, how much comes out, and how groundwater levels and storage are evolving. Better understanding these elements is a fundamental part of managing groundwater sustainably. In overdrafted basins, accounting can go a step further: agencies can establish pumping allocations for individual users to help manage demand effectively. Groundwater allocations facilitate trading and banking water, two approaches that reduce costs for water users and help them manage risk from increasingly intense droughts.

It is difficult to overstate how much the accounting picture has improved over the past six years. The development of GSPs required corralling a lot of the basic information for basins, and GSAs now have annual reporting requirements on key groundwater metrics. To manage their basins, GSAs have also been strengthening their accounting toolkits. GSP implementation started in earnest amid the severe 2020–22 drought, pushing some agencies to fast-track their demand management actions, including new allocation systems. This work has been arduous, but 2023 showed the upside. When the storms came, these agencies were quickly able to establish credits for landowners doing recharge on their farms.

Continued progress is needed. For one thing, only a small (but growing) minority of agencies have allocation and crediting systems. More agencies adopting these systems would facilitate the expansion of landowner recharge on farmland; expanded grower education and better accounting methods would also help. A better picture of valley-wide recharge volumes could be gained through improved tracking of the more informal recharge methods, such as landowner recharge on farmland or via unlined canals and streambeds. Very strong accounting and tracking systems are even more important for developing groundwater banks that store water for off-site parties. The lack of these systems, along with their up-front costs and some regulatory uncertainties, may help explain why we have not seen growth in this area.

Accelerate the Rollout of Recharge on Farmland

In 2017, we flagged the need to remove obstacles that prevent more growers from spreading recharge water on their lands. On a per acre-foot basis, this approach can be much less costly than putting water in recharge basins (M.Cubed 2016), and it can be expanded relatively quickly during very wet years. Obstacles in 2017 included technical issues such as incompatible irrigation systems and concerns about impacts on crop yields, as well as institutional ones such as the lack of incentive programs. In six years, progress has been made on both fronts, and a method that still felt experimental in 2017 has since moved into the mainstream. While the share of agencies that report using these methods has not changed, the total volume of water applied has nearly doubled, and managers reported enthusiastic participation by their growers, especially where groundwater credits and other incentives are in place—and even where on-farm recharge was staunchly opposed in prior years.

Still, the overall contribution of recharge on farmland remains well below potential. To accelerate the rollout, agencies could further expand local recharge tracking and incentive programs, offer more technical support to growers on suitable recharge locations and techniques that are compatible with farm management, and clarify how to manage water quality concerns. Expanding local incentive programs and tapping into federal conservation programs could help offset landowner costs of installing, maintaining, and operating these recharge methods. And especially for growers in groundwater-dependent areas, improvements in the approval process for accessing recharge waters (described above) would make a big difference.

Address Other Regulatory Barriers to Recharge

As in 2017, water managers in our latest survey flagged a number of other regulatory hurdles to recharge beyond getting permission to divert water, such as getting diversion projects permitted (where alignment among regulatory agencies is often an issue), getting water transfers for recharge approved in a timely manner (before the window of opportunity passes), and getting permission to recharge CVP water on non-project lands. We also heard again about price disincentives for recharge with CVP water in a wet year following a prolonged drought, when the CVP is trying to recoup lost revenues. Tackling these various issues will require more institutional coordination and more flexible approaches.

Continue Building Recharge Partnerships

Our 2017 survey took place in SGMA’s early days. GSAs had just been formed, often bringing together parties that were not used to working together to develop GSPs for their basins. At the time, we emphasized the importance of fostering local and regional partnerships to take advantage of recharge opportunities that can benefit multiple parties. Today, it is safe to say that there has been substantial progress on this front, especially at the local level. Many survey respondents mentioned that collaborative recharge efforts are underway or planned with partners in their GSAs or in their basins. These include sharing water, local conveyance infrastructure, and suitable land for recharge. Collaborations between agricultural and urban agencies (and some smaller community systems) are becoming increasingly common. Partnerships are also blossoming between agricultural agencies and their growers, as witnessed by the expansion of landowner incentive programs for recharge.

Since SGMA’s passage, state policy has encouraged these collaborations through funding for SGMA planning and project implementation, with more than $520 million disbursed to local agencies since 2015 (Legislative Analyst’s Office 2024).

Looking ahead, we see two types of recharge partnerships that merit increased attention. The first is projects that can deliver multiple benefits—e.g., providing safe drinking water in underserved communities, reducing flood risk, or expanding wildlife habitat, in addition to storing water for project proponents. There has been growing policy interest in such projects, and new state-funded research on the Merced River watershed offers some of the first quantitative evidence showing the complementarity of recharge and flood mitigation objectives (California Department of Water Resources 2024b). Although current state budget challenges may lower funding for a time, such projects may be more likely to garner both state and federal support. As one example, multi-benefit recharge projects are eligible for funding under the state Department of Conservation’s Multibenefit Land Repurposing Program, which is incentivizing beneficial farmland transitions in critically overdrafted basins.

Groundwater banking projects that store water for off-site parties also merit more attention. This is one of the few recharge activities where we did not see signs of progress between the two survey years. Yet banking partnerships have the potential to help both parties: the off-site partner gets access to a place to store water, and the on-site partner may get both water (the amount that is “left behind”) and funds to help cover project costs. Such partnerships can involve parties from outside the valley—for instance, some Southern California agencies are partners in some of Kern County’s groundwater banks (Escriva-Bou et al. 2020). As noted above, strong monitoring and accounting systems are essential for running these banks, so continued progress in SGMA implementation may foster new banking opportunities.

Conclusion

As PPIC has shown in earlier work, groundwater recharge is the primary supply-side option for cost-effectively reducing groundwater overdraft in the San Joaquin Valley (Escriva-Bou 2019; Hanak et al. 2019). Recharge will also become increasingly important for this region in our changing climate, as droughts become more intense (Albano et al. 2022; Moyers et al 2024), rising temperatures reduce seasonal storage of water in mountain snowpack (Shulgina et al. 2023), and larger storms increase flood risk (Swain et al. 2018). Strong progress on recharge is key, both to minimize reductions in water use and irrigated acreage as the valley implements SGMA, and to mitigate growing risks from both droughts and floods.

In many regards, 2023 was a banner year for recharge in the valley, reflecting momentum since the wet winter of 2017 from both the implementation and policy standpoints. Volumes are up, interest in recharge remains high, some of the technical difficulties have been ironed out, and both local and state policies are evolving to reflect accumulating on-the-ground experience. But more work is needed to realize the promise of this tool. Two major efforts require the robust involvement of state agencies and local stakeholders: conducting broad, watershed-scale assessments of the conditions under which water can be made available for recharge, and evaluating where improvements in regional conveyance infrastructure would be good investments.

Making continued, incremental progress in several other key areas—including groundwater accounting, recharge on farmland, regulatory flexibility, and recharge partnerships—will help the valley secure a sustainable future for its people, economy, and environment.

Topics

Drought Floods San Joaquin Valley Water Supply Water, Land & AirLearn More

How Much Water Is Available for Groundwater Recharge in the Central Valley?

Making Recharge a “Win-Win” for Landowners and Groundwater Agencies

Groundwater in California

Video: Replenishing Groundwater in the San Joaquin Valley

Commentary: The San Joaquin Valley Pumps Too Much Water. But There Are Signs of Progress

Understanding Water Available for Recharge in the Central Valley

Replenishing Groundwater in the San Joaquin Valley